| Highlights: Switching a property from residential/long-term rental to short-term rental use, such as through Airbnb, can trigger significant GST/HST liabilities upon sale. The change-in-use rule under the Excise tax Act applies to a property when it transitions to short-term rental use making it taxable on sale. If more than 90% of a property’s usage is for short-term rentals and the property is rented out for less than 28 days, In the case of 1351231 Ontario Inc. v. The King, courts decided that even brief use of a property for short-term rentals led to an $80,000 HST reassessment Property owners must understand timing rules, potential liabilities, and strategies to minimize unexpected costs and maintain profitability. |

Introduction

As the real estate market evolves and new income opportunities emerge, understanding the tax implications of switching property use has become crucial. Switching your property to be used for short-term rentals, like Airbnb, might seem like a valuable business opportunity, but it carries significant financial risks. Before taking this avenue, it is important to understand Canada’s GST/HST laws and how they apply to your property. Owners who use properties for short-term rentals must be aware of the tax liabilities they may face upon the sale of their property. Failure to consider these implications could lead to unexpected tax liabilities. This article explores how these tax regulations might affect you as a property owner.

When Does GST/HST Apply to Your Property Sale?

Typically, selling a used residential property in Canada is exempt from GST/HST taxes even when it is used as a long-term rental. GST (Goods and Services Tax) and HST (Harmonized Sales Tax) are consumption taxes levied on most goods and services in Canada. Owners of rental properties must understand how these taxes apply, particularly when properties are used for short-term rentals.

If a property has been used to generate taxable income, as a hotel, motel, AirBnb, or other short-term rentals, the sale may suddenly become subject to GST/HST. This can be a costly surprise for landlords. HST applies if:

In these cases, your property might be treated as a commercial asset, which could result in HST being charged when you sell the property. If a property owner transitions from offering long-term rentals to short-term stays (e.g., listing a property on platforms like Airbnb), the GST/HST change-in-use rule found in subsection 206(2) of Canada’s Excise Tax Act applies.

Change-in-Use Rule – subsection 206(2) of Canada’s Excise Tax Act

This rule states that when a property’s use changes to a taxable purpose, which means from long-term rental or residential to short-term rental, the owner is deemed to have “repurchased” the property at its current value.

What Qualifies as Change in Use?

If you decide to switch a property’s use from primarily long-term rental use to short-term rental use, you will inadvertently trigger GST/HST liability on the ‘deemed value’ upon sale.

This triggering of this tax liability was demonstrated clearly in the recent case of 1351231 Ontario Inc. v. The King (2024).

Case Study: 1351231 Ontario Inc. v. The King (2024)

A recent ruling from August 2024 clarifies that short-term rental activities can change the tax treatment of a property from exempt to taxable under Subsection 206(2) of the Excise Tax Act.

The case of 1351231 Ontario Inc. v. The King provides an eye-opening example. Here’s what happened:

The Final Outcome?

The CRA reassessed the sale as taxable, imposing $80,000 in GST/HST as there was a change of use under section 206 of the Excise Tax Act. The Tax Court upheld this decision, noting that the property’s use for short-term rentals, even briefly, disqualified it from GST/HST exemption at the point of sale.

Key Takeaways from this Case

This case clarifies several points for us on the topic of HST on sales of properties being used for short-term rentals.

Pro Tax Tips for Property Owners

Conclusion

Selling a property used primarily for short-term rentals in Canada can trigger significant HST implications, and it’s an area where property owners need to tread carefully. Under Canadian tax rules, rental income from short-term stays—defined as less than 28 consecutive days—is taxable. If more than 90% of the property’s use involves short-term rentals, the property may be categorized as a commercial asset. This change in use as per Canada’s Excise Tax Act can make the property’s sale subject to HST, potentially leading to a hefty and unexpected HST liability.

For property owners and real estate investors, these tax implications highlight the need for thorough tax planning and professional legal advice. An experienced real estate lawyer can help you understand how these rules apply to your situation, ensure compliance, and explore opportunities to mitigate tax liabilities. Given the complexities and potential for costly reassessments, proactive tax advice is crucial. Proper planning can make a significant difference in preserving your investment’s profitability and navigating Canada’s real estate market with confidence.

Canada’s housing market has experienced significant volatility and change in recent years. A lot of factors have propelled the big spike in real estate prices that we saw in 2021, followed by the decline in the last couple of years, to where we are now in 2024. The factors that are discussed in this article are not just periodic, but they consistently have an influence on the real estate market. Having knowledge of these factors will help you understand the direction of real estate prices in the future. This article provides you with a deeper understanding behind the home prices that you see under a listing. Being aware of these factors can help you be a better investor and make more confident real estate decisions.

The first factor is a major one and it is the economic factor. The news often discusses Gross Domestic Product (GDP) and inflation. It may surprise you to know we’ve had greater inflation in the last few years than we’ve seen in 40 years! Target rates of inflation have usually been 2-3% but in the last couple of years, we have been over that 3% mark. This becomes clearly visible when we walk into the grocery store. The same amount of groceries from three years ago are costing people over 20% more today! How is that relevant to the real estate market? Well, in fact, that affects an average Canadian’s ability to save money for the purchase of a home, affecting the affordability of home buyers.

Making the headlines of the news periodically in the last few years are the Bank of Canada changes in interest rates. A-level mortgage financing went up to 5-6%, B-level mortgage financing is well over 6% and private could be up to 15% depending on the lender. When we see interest rates increasing, it’s important to keep in mind that the same demand remains for the properties in the market. However, as previously discussed, the affordability of home buyers has changed drastically as their income levels remain the same. Buyers are not positioned to deal with the interest rate increase. This poses a problem for the sellers and buyers. The sellers still need to sell. The buyers still need to buy. However, potential real estate transactions are stuck because of a big gap between the reasonable sale price for the seller and an affordable purchase price for the buyer. It has become difficult to find the midpoint where both parties would find the transaction worth it.

The third factor which arises from the increases in interest rates and lack of affordability, is increasing supply. Real estate transactions sit on supply and demand. As properties sit on the market a lot longer with a lack of transactions taking place, more properties come every month to add to that supply. The properties that sit in the market for longer must demand for a lower price point. However, sellers that put their property on sale still need to operate on the same timeline that is motivating them to sell. Whether that’s a new job, purchase of a new property, or the lack of affordability in keeping the property due to the hike in interest rates. The market is inevitably conditioning a situation where a seller must sell, but the buyer may or may not buy. Buyers now have more options in the housing market even though their mortgage interest rates are high because of the increase in supply. With the buyer’s having more choice than the seller, this forces home prices down.

Another factor affecting housing prices in 2024 is government policies. Government policies include things like zoning, taxes, foreign buyer taxes, and stress tests, that have all been affecting the housing market for the past few years. These government policies are affecting real estate prices today. The foreign buyer tax was designed to bring prices down because it places barriers against money coming in from foreign sources. This should ideally drive the prices down for domestic home buyers. However, this gets in the way of more money coming into the housing market, which affects funding for building projects. On top of less funding for building projects, we are heavily regulated by building permits and standards in Canada. This reduces supply in the housing market and increases prices of preconstruction properties, cycling back to causing unaffordability for home buyers.

The reduction in housing supply becomes a significant problem as Canada consistently welcomes a record-breaking number of immigrants each year. High levels of immigration and population growth contribute to increased demand for housing, particularly in urban centers like Toronto, Vancouver, and Montreal. These cities are popular among immigrants due to the job market, existing cultural communities, and established settlement services. The increased demand that comes with population growth can drive up home prices and rent prices, especially in markets where the housing supply is already constrained. This fast-growing demand is met with a slow lagging of housing supply caused by the already discussed limited funding for building projects, slow construction processes, and strict zoning regulations. Government policies that promote immigration, such as programs targeting skilled workers and international students, further amplify this effect by continually boosting population growth. For example, Ontario’s Provincial Nominee Program (PNP), which enables the province to choose immigrants based on specific economic requirements in the region, has been highly successful in drawing skilled workers. As this may strengthen the local economy, it elevates the demand in the Ontario housing market and drives up home prices for everyone.

Housing prices in 2024 are influenced by a complex web of factors that continually shift supply and demand, shaping the market’s overall direction. Economic conditions such as GDP growth and inflation play a significant role, as they impact overall home buyer affordability. The rising interest rates have added another layer of pressure for home buyers, further reducing affordability. This situation is met by an increased urgency among sellers to sell their properties that have been sitting on the market for a long time. On the other hand, stringent government policies that regulate real estate development reduce housing availability, and the housing market is unable to meet the demand driven by drastic population growth that comes with immigration. Understanding these intertwined factors is crucial for navigating the current and future landscape of the real estate market.

For investors, homebuyers, and sellers alike, being aware of these market influences can help anticipate potential shifts and prepare for upcoming changes. This awareness enables stakeholders to make strategic decisions, whether it’s timing a property sale, identifying investment opportunities, or securing a new home. By staying informed, you can better position yourself for success in the ever-evolving real estate market in Canada.

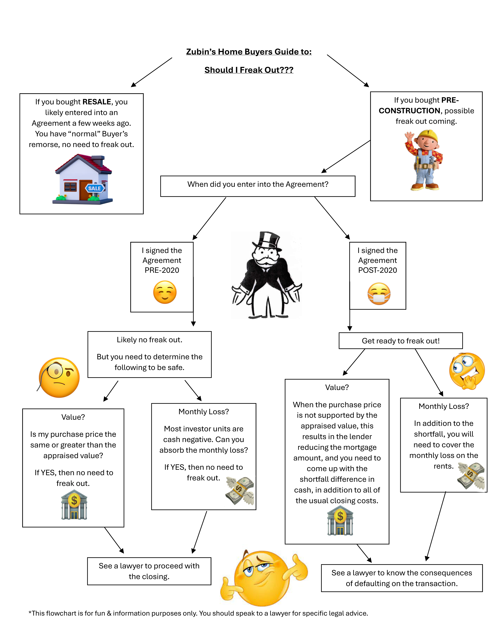

Buying a home is one of the biggest investments you’ll ever make, and it’s natural to feel anxious. But before you panic, take a moment to assess your situation using Zubin’s Home Buyers Guide.

If you recently bought a resale property, there’s no need to worry! Most of the time, the buyer’s remorse you’re feeling is entirely normal. However, if you signed the agreement prior to 2020, it’s still important to double-check a couple of things:

Pre-construction buyers, it’s time to brace yourself. Post-2020 agreements might present a few challenges:

In both scenarios, if the value or monthly losses don’t add up, it’s crucial to speak to a lawyer. They can help you navigate closing challenges or understand the consequences of defaulting on the transaction.

Highlights

All Ontario real estate owners need to be aware of the recent change implemented by the government in relation to Notice of Security of Interests. The new Homeowner Protection Act 2024 introduced on June 6, 2024, made significant changes to the registration and enforcement of Notice of Security of Interests in Ontario. Creditors will no longer be able to register their security interests on title to the properties where consumer goods are installed as chattels or fixtures. This article will introduce you to these changes in the law and highlight the impacts that comes as a result.

A Notice of Security of Interest (NOSI) is a lien registered on title notifying the public of an interest of a creditor in the personal property. This provides security to a creditor who allows the property owner to rent certain equipment and fixtures. The Notice of Security of Interest is recorded in the Land Registry System so that a creditor is protected upon the sale or refinancing of the property. The registration notifies anyone with existing or future interest in the property that a specific fixture on the premises is encumbered by a security interest. Consumers are often unaware of the registration on title when they rent the equipment. It only comes to light during the purchase, sale, or refinance of a property as lawyers conduct a title search on the property. Equipment on the property that requires a NOSI includes water heaters, air conditioners, furnaces, water softeners, water purifiers, etc.

There are two major effects that come from the Homeowner Protection Act 2024.

The first effect being that the NOSI can no longer be registered against the property where consumer goods are concerned. As per Section 1 of the Ontario’s Personal Property Security Act, “consumer goods” are “goods that are primarily used or acquired for personal, family or household purposes”.

The second effect being that existing registered NOSIs registered as of and prior to June 5, 2024, are considered expired. These are no longer of effect, and they may be deleted by an application submitted by your solicitor subject to legal fees & disbursements.

If a new NOSI is not in relation to consumer goods, this must be confirmed by a statement signed by a lawyer. In such cases, the NOSI will be registered pursuant to section 54 of Ontario’s Personal Property Security Act.

Following these changes in the law, creditors would have to pursue by independent means of enforcing their security interests. Where creditors were able to wait for the sale or refinance of a property to recover their payment, they now will have to begin legal proceedings to enforce their debts. They would have to wait to obtain judgements in these proceedings and register writs of executions on title. This places consumers in the same position as before but consumers would incur significant additional costs as per the rules of the court.

The alternate route that creditors can take to enforce security is by seizure and sale as per the Personal Property Security Act (PPSA). The collateral concerned in many cases is HVAC equipment and the disruption caused by such harsh enforcement will result in the consumer incurring significant additional costs.

Many creditors also would turn to reporting consumer defaults to credit reporting agencies. This would then remain on the consumer’s credit report for a seven-year period despite the resolution of all defaults. This would not be a route for the creditor if the option to passively enforce the default through NOSI existed.

Creating a transparent real estate market allows homeowners to protect their interests and buyers to make fully informed decisions. Being aware of the new changes in the law is essential for ensuring the legality of any property transaction. As proactive real estate lawyers in Toronto, we prioritize keeping our clients updated on the latest legal developments. At Bradshaw & Mancherjee, we ensure that your real estate transactions are secure, legally compliant, and successful.

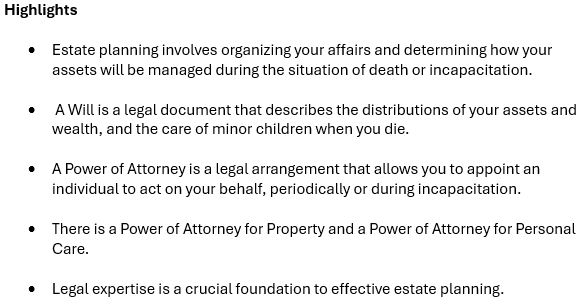

Estate planning is essential for every individual to secure their personal and financial legacy. To ensure that your wishes are honoured, and your loved ones are taken care of, it is important that your Will and Power of Attorneys are well-crafted and in place. Estate planning involves taking the proactive step of organizing your affairs and determining how your assets will be managed and distributed in the event of incapacitation or death. This article will delve into the importance of these elements and how they contribute to a comprehensive estate plan.

A Will provides you with peace of mind, knowing that your estate is managed intentionally, while minimizing potential legal and financial complications in your absence. A Will, also known as a Last Will and Testament, is a legal document that describes your intentions for the distributions of your assets and wealth, and the care of any minor children after your death.

Being the cornerstone of your estate plan, a Will gives you the powers to name executors, specify bequests, appoint guardians, and establish trusts for your beneficiaries. Here are some of the key elements involved in crafting your Will:

Executor/trustee: a legal representative chosen to administer an estate upon your passing.

Beneficiary: an individual or organization that is receiving some or all of your assets and property upon your passing.

Bequest: a provision in your will that allows you to allocate specific assets to beneficiaries or charity organizations named in your will.

Custodian: an individual responsible for the care and upbringing of your dependants or minor children if you pass away.

Testamentary Trust: a legal arrangement that holds money, property, or personal items for beneficiaries by managing assets based on the directions in your will.

Should you fail to establish a Will that secures the future of your estate, your estate will be distributed without your freedom of choice in accordance with Ontario’s Succession Law Reform Act.

A Power of Attorney is an important legal arrangement that allows you to appoint an individual to act on your behalf while you remain alive. As a grantor, you would be able to appoint an attorney to ensure that your affairs are managed smoothly and in accordance with your wishes and best interests. Your attorney is trusted with the responsibility of making significant decisions when you become mentally or physically incapacitated. There are two types of Power of Attorneys in Ontario: Power of Attorney for Property and Power of Attorney for Personal Care.

Grantor: The person who makes a power of attorney and appoints another to act on their behalf.

Attorney: The person you appoint to act on your behalf.

The Power of Attorney for Property grants the attorney with the power to make decisions regarding finances on your behalf. As a continuing/enduring power of attorney, the attorney can exercise this authority when you are no longer mentally capable of managing your affairs. As a non-continuing power of attorney, the attorney can exercise this authority while you are still mentally capable of managing your financial affairs. For example, if you are away from home for an extended period of time, you may appoint someone as your attorney to look after your financial affairs.

An attorney is empowered with the authority to do almost anything with your finances. This includes:

The Power of Attorney for Personal Care involves making health care and personal decisions for you. These are important decisions surrounding medical treatments, living arrangements and palliative (life-support stage) matters.

In Ontario, there are a few requirements that must be met in order to appoint one as a power of attorney.

The attorney must be:

When more than one person is acting as authority, you can grant them authority to act independently under several authority, or the individuals chosen can also act together under joint authority.

Now that you have a brief overview of Wills & Power of Attorneys. We are going to begin eliminating some common misconceptions.

Once you reach the age of 18, it is important to draft a Will even if you don’t own a lot of financial assets or have children. All Canadian adults should have a Will and Power of Attorneys to secure their future. Having a Will ready illustrates what your loved ones should do in the event you pass away. No matter how old you are, life is never a certainty, and things can happen unexpectedly. By having a Will in place, you can be ready, protected, and have peace of mind.

Your estate will be distributed based on Ontario’s Succession Law Reform Act if you pass away without a Will. This means that you do not have the ability to fully exercise the freedom to allocate your assets as you please. This could leave spouses, common-law partners, or other loved ones vulnerable as assets would not be distributed according to your intentions.

There are many Will templates offered online for different prices. However, if the correct legal language is not used in your Will, your Will could be ruled invalid, and your estate would be handled by the courts as if you had no Will. You may also be unaware of witnessing and other requirements without which your Will would be legally invalid.

More complicated estates may not be sufficiently handled by the templates available online. For example, if you own a business, own multiple properties, have complicated family dynamics, or significant assets, an estate lawyer would be able to provide you with constructive and tax-effective strategies based on their legal expertise.

Why would you risk losing your ability to choose what happens after your passing? To ensure that your Will and Power of Attorneys are both legally valid and effective, the best thing to do is hire an estate lawyer.

An individual’s legacy and security of their loved ones are built on a well-structured estate plan. After facing the difficult time of losing you, your family should not be burdened with the confusion of how to handle your financial and personal affairs. With our firm’s meticulous attention to detail and deep understanding of the law, we ensure that our clients’ assets are protected, their intentions are honoured, and their beneficiaries are looked after well. At Bradshaw & Mancherjee, our expertise in drafting wills and creating power of attorneys allows us to tailor legal strategies that meet the unique needs of each client. As estate lawyers in Toronto, we take pride in our role of safeguarding the legacies of those we serve, making estate planning an integral part of our practice.

There are various financial complexities that come with a home purchase. Understanding the associated costs is crucial in determining the steps you should take in your real estate transaction. This article provides a comprehensive overview of closings costs, including mortgage and property-related fees. These costs can add up quite quickly, so it is important to educate yourself of these costs before stepping into a real estate transaction.

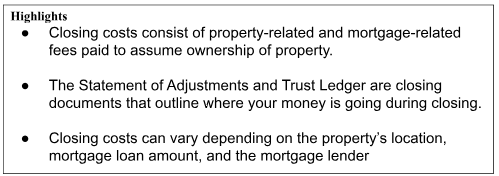

Closing costs are the administrative and legal fees associated with a real estate transaction. These costs can vary significantly depending on the property’s location, mortgage loan amount, and the mortgage provider. Here is a brief closing cost breakdown to provide you with a little homebuyer assistance.

Title insurance: If you intend on purchasing your property with a mortgage, one of the conditions in your mortgage commitment will require that you obtain a title insurance policy. This is a one-time fee paid at closing and the policy remains active throughout the duration of your home ownership.

Land Transfer Tax: This tax is payable for any purchase of real estate, including condominiums, cooperative apartments, and vacant land in Ontario and other provinces. The amount of the tax increases as the purchase price increases. Some cities, such as Toronto, also have a municipal Land Transfer Tax.

Home inspection fee: The buyer is expected to cover the cost of home inspection. Home inspection is not required but it is highly recommended as they often reveal major structural issues that the buyer should be aware of before completing the transaction. These issues are usually not simply noticed by walking through the house with a realtor.

Survey fee: Mortgage lenders typically require a land survey to be presented by the seller to the homebuyer. If a survey exists, it will be handed over to you by the seller. This is a map of a property’s boundaries outlining the beginning and end of a property’s borders. If the seller does not have a survey, the homebuyer may be required to pay for one.

Legal fees: These fees cover services such as title searches, contract reviews, and document preparation, which are provided by the real estate lawyer. They vary depending on the complexity of the transaction and the expenses involving title insurance, land registry fees, and courier fees that the lawyer incurs while representing you on the transaction.

Homeowners Insurance: Securing home insurance coverage is vital for your property. It is essential for you to obtain home insurance coverage effective as of the proposed closing date and it is a necessary cost for closing. If you are obtaining a mortgage, your lender’s interest as first loss payee must be noted on the property. Prior to closing, we must receive a copy of your policy or binder letter.

Pro-rated property taxes: When buying a new home, your lawyer will confirm that all of the seller’s expenses have been covered up until the closing date, including property taxes. If the seller is not up-to-date with the property taxes, they must pay the outstanding balance to the municipality. However, if the seller is ahead and paid the taxes for the year, the buyer must reimburse the seller for the amount paid between the closing date and end of the prepaid period.

Home appraisal fee: A conventional mortgage requires the order of an appraisal on the home being purchased. This mortgage-related fee is for lenders to verify that the property you are securing a mortgage against is worth the value being paid for it. By conducting an appraisal, lenders can provide you with accurate loan estimates. Going forward, any mortgage refinancing done on the property would be subject to a home appraisal fee as the value of any home changes over time.

PST on CHMC-insured premium: CMHC (Canada Mortgage and Housing Corporation) Insurance protects lenders if borrowers ever default on their mortgage. This is required if you are not able to make a down payment of 20% or more on the home you wish to purchase. This cost is added to your mortgage and paid over the course of the mortgage loan. However, there is a Provincial Sales Tax (PST) associated with CHMC that must be paid for upfront. In Ontario, the PST on CHMC Insurance is 8%.

For example, if the CHMC Insurance Premium is $6200 with the 8% tax rate in Ontario, the PST owed would be $496. This would be paid on closing day.

This article provides you with a concise summary of some of the general costs associated with the purchase of a home. However, there may be fees subject to your particular real estate transaction. On the day of closing, your lawyer will guide you through the Statement of Adjustments as well as the Trust Ledger Statement, which will provide you with an accurate picture of the costs associated with your transaction.

The statement of adjustments outlines a list of debits of amounts already paid (such as the deposit) and a list of credits (such as the purchase price and prepaid fees on the property). The credit column subtracted from the debit column provides you with the amount owed to the seller on the closing date.

The trust ledger takes the amount you owe to the seller and outlines how the amount is allocated. The list of credits includes the loan amount from the lender and your down payment. The list of debits outlines where all of that money is going and how it will cover the different closing expenses.

Buying a home is a significant life decision and it is important that buyers do not walk into this decision blindsided. Navigating the closing costs associated with purchasing a home can be complicated, which is why you require the expertise of a real estate lawyer to guide you through the process. At Bradshaw & Mancherjee, we provide you with the support and knowledge you need to make informed and confident decisions about the purchase of your home.

A recent phenomenon that we are starting to observe in the real estate market is the brutal state of condo assignment sellers. An increasing number of pre-construction condo assignors in the GTA are facing major difficulties in closing deals. This shortfall is triggering a sell-off, with unit prices dropping and sellers losing all of their deposit and more! First of all, what is an assignment sale?

An assignment sale is a type of real estate transaction that with pre-construction properties. This is where the original buyer transfers their rights and obligations under the Agreement of Purchase and Sale to a new buyer, before closing or taking possession of the property. The new buyer then steps into the original buyer’s position and completes the deal directly with the builder.

In a market where all odds are against the assignor, it is important for assignors to be aware of the heavy competition surrounding them. There are desperate assignment sellers who bought units that they cannot afford to close and there is more assignment inventory than there has ever been. To top it off, there are even more resale condos on the market than there has been in the past decade. That means the only way to succeed at an assignment sale is to make the unit better priced than other competing assignment listings AND the resale market. This surge in assignment availability has driven unit prices to take a major plunge below the original purchase price. Consequently, assignment sellers are often forced to accept significantly lower offers than anticipated. Not only failing to make profit but facing extensive loss out of their own pockets.

The interest in assignment flipping really escalated after the year of 2020 due to its belief of high profitability. Stories of people making hundreds of thousands of dollars without closing between 2018-2020 circulated through the market. Family, friends, and realtors passed along such anecdotes gambling their interests without being fully aware of the risks involved.

In the midst of this dilemma, appraisals are serving as the safety blanket for newly completed condo units, providing them with value and allowing people to close. When observing the prices of resale condos between the years of 2018 to 2024, it can be seen that the price per sqft remains the same, that is $1000/sqft. That is zero nominal change in a period of six years! This is a whole building cycle for pre-construction properties. Pre-construction condos purchased in those years are worth way more than $1000/sqft with closings coming up in 2025 and onwards. In this situation, if appraisals don’t come in, then the average investor would not have hundreds of thousands of dollars to make up for the substantial shortfall.

Another trend that we can observe in the preconstruction market is the steep decline in projected completions as presales are not happening. The only people active in the preconstruction market right now are end users, people who are buying to downsize or upsize. However, it is worth pointing out that end users only make up 20-30% of the pre-construction buying pool and the rest are investors. This is because end users don’t want to wait 5 or 6 years for their unit to complete, so they are more active in the resale market. Less investors active in the pre-construction market means that there will be much less project completions in the future.

What does this mean for the real estate market? This means that we have a real supply issue for the future if our population continues to grow at this rate, as the fastest growing metropolitan area in North America. However, waiting for this demand to play out is not a solution for the dilemma in assignment sales today. This phenomenon may take longer than expected to come to play.

Assignors are backed into a corner in the situation of today’s market. Assignors are forced into a situation of selling at a loss, and refusing to sell at a loss means that they are forced into closing as the buyers of the unit. Either way, assignors in the pre-construction condo market are finding themselves in a tough spot.

With the dynamic nature of Ontario’s real estate market, things do not always go as planned from the initial agreement to the final closing. However, it is important to remember that the Agreement of Purchase and Sale is a legally binding contract. This means that there are legal implications for all the parties involved when certain parties choose to withdraw from the agreement. Depending on whether they are the buyer or seller, parties are vulnerable to significant legal and financial consequences. This article will uncover the legal and financial consequences facing sellers who choose to withdraw from real estate contracts as per Ontario real estate law.

Seller’s remorse is a real phenomenon. It happens when the seller believes they made a mistake in selling their home. They may face regret for not making enough money from the sale of their property, missing their old neighbourhood, or simply just regretting the decision to sell in that particular point in time. The court’s response to seller’s remorse is not generally a favourable one and it is not a legally recognized reason for breaching an agreement. In these circumstances, sellers may face legal disputes or financial penalties.

In order to understand legal implications, one needs to understand the legal footing of real estate contracts in Ontario. Upon signing the property sale agreements, both the buyer and sellers are obligated to fulfil the terms outlined in the contract. The primary duty of the seller is transferring the ownership of the property to the buyer by the stated closing date. Further duties of the seller are outlined in the contract for the period of due diligence, from when the contract is signed up until the closing of the property. During this period, the buyer is given an opportunity to conduct an appraisal, a title search, organize their mortgage, perform property inspections. Meanwhile, the seller has the obligation of maintaining the property in the condition it was agreed upon for closing, providing access for inspections, clearing encumbrances, and conducting agreed-upon repairs or modifications on the property before the closing date.

Sellers backing out of an APS face detrimental consequences for contract cancellation. Ontario property law is sincere in upholding its duty of protecting both buyers and sellers’ rights in real estate transactions. During a real estate closing, seller obligations must be upheld to avoid seller penalties. When the seller breaches the agreement, legal recourse is readily available to the buyer. This could involve potential lawsuits for damages, specific performance, losing the deposit, or reimbursement costs involved in the execution of the agreement of purchase and sale. A buyer has the right to seek damages from the seller in courts, where the seller would owe monetary compensation for any losses incurred by the seller’s contract termination. By requesting specific performance, buyers can have the court forcefully order the seller to sell their property in honour of the purchase and sale agreement. Buyers can also have the costs involved in the property purchase process recovered at the expense of the seller if the closing process cannot be completed due to the seller. Such costs include inspection fees, legal fees and moving costs.

The breach of a real estate contract is not immediately sent to court for resolution.

Real estate disputes that occur through contract breach are usually first attempted to be resolved through negotiation between the buyer and seller. There may be a possibility that the parties themselves come to a compromise that prevents the breach of the agreement.

Next, to avoid the time and expense of a court case, the parties may reach a settlement through mediation, where a neutral third party helps to facilitate a mutually agreeable resolution.

Finally, If the conflict fails to be resolved through mediation, parties may decide to proceed with court litigation. This is when courts will intervene and decide the consequences depending on buyer’s rights and seller’s rights outlined in the law and with the consideration of the terms in the agreement of purchase and salw.

To prevent seller’s remorse and the significant legal and financial repercussions that sellers may face in breach of contract, there are some basic steps you can take:

We can help you!

Fortunately, these are all precautions that our legal team at Bradshaw & Mancherjee would be happy to assist you with. Our proficient experience in the field of real estate law means we specialize in protecting both sellers and buyers.

With our meticulous attention to detail, we will review your contract for potential contract contingencies, negotiate terms that safeguard your interests, and represent you in disputes that may arise in the course of your real estate transaction. Bradshaw & Mancherjee offers strategic advice and legal solutions tailored to protect sellers’ interests and navigate complex contractual obligations in Ontario.

By working with our team of professionals, you can make confident real estate decisions every step of the way. For any inquiries you may have or to schedule an appointment with one of our expert legal professionals, please feel free to contact us.

The Ontario real estate market is dynamic and constantly changing. Navigating the intricacies involved in open bidding and real estate auctions requires a thorough understanding of the underlying legal framework. We help buyers, sellers, and investors make informed and confident decisions. The expertise and comprehensive legal guidance provided by our lawyers at Bradshaw & Mancherjee will help you succeed in the competitive real estate arena. This article explores the dynamics of open bidding and auctions surrounded by the complexities of Ontario real estate law and essential tips for thriving in this competitive market.

All real estate transactions involving the purchase, sale, and leasing of properties are governed by Ontario real estate law. This law ensures fair and transparent transactions between buyers and sellers through a wide range of regulations. Whether you are a first-time homebuyer or an experienced investor, understanding these laws is essential for all of those who participate in the field of real estate.

Open bidding in real estate is when an offer for a property is proposed by potential buyers and accepted by potential sellers through a transparent bidding process. In contrast to closed bidding, open bidding allows for potential buyers to be aware of all competing bid details, including the purchase price, financing, market activity and terms. Potential buyers are given the opportunity to make informed adjustments regarding their offers accordingly. With increased transparency, a real estate competition is fostered, and this often causes a surge in sale prices of properties. True market demand is demonstrated, providing sellers with a realistic idea of their property’s value.

High-demand properties may utilise the method of real estate auctions for property sales. In a real estate auction, properties are sold to the highest bidder through a competitive bidding process open to the public. These auctions take place in-person or online and consists of the participation of bidders, auctioneers, and sellers. Successful auction strategies require an understanding of certain dynamics in the auction process such as the reserve price, bidder behaviour, and auctioneer’s role. The reserve price is the minimum price that the seller is willing to accept from potential bidders. Bidder behaviour, that is the way bidders interact with one another and strategize, creates the atmosphere of the auction. The auctioneer is responsible for managing the process, ensuring the rules are followed, and encouraging bids from bidders.

Auction houses are the establishments that facilitate the sale of real estate properties. Understanding auction house procedures can help you be prepared and navigate the process effectively. Some important procedures that take place within the auction house include:

While both open bidding and auctions involve competitive bidding, there are some key differences between both methods. They vary in transparency, where open bidding is completely transparent, but auctions may or may not publicly reveal all bids. Auctions are fast-paced and conclude in a short period of time, but open bidding can continue over multiple days or weeks for a particular property.

How to handle bidding wars in real estate

Bidding wars are a common phenomenon in competitive real estate markets like Ontario. Successfully navigating a bidding war requires a clear strategy and the ability to remain calm under pressure. Below we offer some quick buyer and seller auction tips that you can use in bidding wars.

There are strict regulations put in place to govern Ontario property auctions and ensure fairness and transparency in transactions. The auction law in Ontario is enforced by the Real Estate Council of Ontario (RECO). This body oversees the regulation of real estate auctions, ensuring compliance with the Real Estate and Business Brokers Act (REBBA). These rules cover the conduct of auctioneers and outline the rights and responsibilities of buyers and sellers. Some of the aspects dealt with in these auction regulations are the disclosure of property information, the setting of reserve prices, and the management of deposits and payments. Being a participant in the real estate bidding process makes it essential for you to understand the legal implications of your actions. This includes knowing your rights and obligations for property bidding in Ontario, understanding the terms of the sale, and being aware of any circumstances that may affect the transaction.

Our lawyers have extensive experience in Ontario real estate law and have the expertise to guide clients through the intricacies of auction dynamics. We will guide you through all the legal aspects of bidding that you need to be aware of to make confident and well-informed decisions. For example, one of these aspects are disclosure requirements, which require all the relevant property information to be provided to potential buyers. Auctioneer conduct is governed by such regulations, where auctioneers must have a valid license and they must act according to specific ethical standards. There are also particular bid handling rules that entail how bids are received, recorded, and accepted. From understanding real estate auction rules to developing auction strategies and giving you great real estate bidding tips, we ensure that you are empowered to make informed decisions to achieve your real estate goals.

Achieving success in real estate bidding requires the right expertise and guidance. Our team of professionals can assist you in making informed decisions and help you secure the best possible outcomes. Contact Bradshaw & Mancherjee today to learn how our specialized real estate lawyers can assist you in the competitive Ontario real estate market.

Buying a home? Congratulations! It’s exciting, but there is a lot of documentation. A notary public is essential to the success of your real estate transaction.

Every detail matters in real estate transactions, from the first contract to the last important exchange. Notary services are essential to guaranteeing the security and legality of these transactions. Due to the intricacy of real estate transactions in Ontario, notaries are frequently needed to formalize and verify the multitude of papers needed.

Let’s check the role of notaries and highlight little-known but important details of real estate transactions.

Notaries public are licensed legal professionals in Ontario who can witness signatures, confirm the parties’ names, and give legal standing to documents including mortgages, powers of attorney, and deeds. They protect against fraud and forgery by signing and sealing the documents with their official seal. This is especially important when there is a lot on the line, such as when large amounts of money or valuable property are being transacted.

Although notary services are provided by banks, they are often restricted to transactions involving specific clients. Independent legal professionals are recommended for comprehensive real estate transactions, which require unbiased legal oversight. These lawyers guarantee that all legal obligations are fulfilled without any potential conflicts of interest that may occur in a banking setting.

In Ontario, the lawfulness of remote notarization has changed, especially because of the current trend toward digital alternatives. These services combine the ease of remote processing with the security of in-person notarization. They are especially helpful for those who are unable to visit in person. However, in-person notarization may still be necessary for some essential documents to satisfy particular legal nuances, particularly those involving large transactions like real estate.

Ensure your documents are legally binding and compliant with professional notary public services. The cost of notary services varies according to the kind and quantity of papers.

A notarization, including the notary’s stamp and signature, costs $37.99 plus HST for up to 20 pages requiring a single notarization. Although some could argue that these costs are unnecessary, they are essential for comprehensive legal verification and provide a level of protection that exceeds their expense. These are usually simple fees that are expected to be included in the closing expenses of a real estate transaction.

Our experienced team provides comprehensive document certification and notarization services at competitive prices. Book your notary appointment today to secure the authenticity and legal validity of your important documents with ease.

For more details on the costs involved in purchasing a new home, visit our page on New Home Cost.

Using notary services in North York has several benefits. They guarantee that:

The likelihood of future legal disputes arising from property ownership or terminology misunderstandings is greatly decreased by this procedure.

Here’s a list of typical documents that commonly need a notary’s touch:

Notaries help make sure these important documents are done correctly and are legally binding. This prevents fraud and makes sure the document can be used in court if needed.

A real estate transaction’s closing phases are crucial. For example, notarizing the closing paperwork guarantees the legal recognition of the property transfer. Clients may plan their relocation more effectively if they are aware of the key collection timeframe and process, which are explained in ‘When do I get the keys?’ Hiring a skilled notary is essential since delays in notarization might cause relocation plans to be affected by the delivery of keys being postponed.

A real estate transaction’s closing phases are crucial. For example, notarizing the closing paperwork guarantees the legal recognition of the property transfer.

Clients may plan their transfer more effectively if they are aware of the main collection timetable and procedure, which were previously explained. Hiring a skilled notary is essential since delays in notarization might cause relocation plans to be affected by delayed delivery of keys.

Without an experienced notary, navigating the intricacies of real estate transactions can leave parties vulnerable to legal risks. Both individuals and companies may ensure that their real estate transactions in Ontario are safe and compliant with the law by being aware of the functions and advantages of notary services.

In Ontario, are you starting a real estate transaction? With our skilled notary services, you can protect your investment and feel at ease. Get in touch with us right now for thorough assistance with your real estate endeavours.